COVID 19’s Impact on The U.S. Bank Industry Performance

The impact of COVID 19 on the global economy has been devastating, but the impact on the U.S. economy may be less significant in large part to the pivotal role the U.S. plays as the world’s leading economy and the strengthening our economy experienced in recent years. Also important was the federal government’s response to the shutdown in providing funds to individuals and businesses. The vital role of U.S. banks in the implementation of the government programs cannot be overstated and it may be assumed by some that the banks benefited from these programs in the form of increased business activity at a time when most businesses saw dramatic declines in business activity. The question is, how was the performance of U.S. banks impacted by the economic shutdowns imposed because of COVID 19?

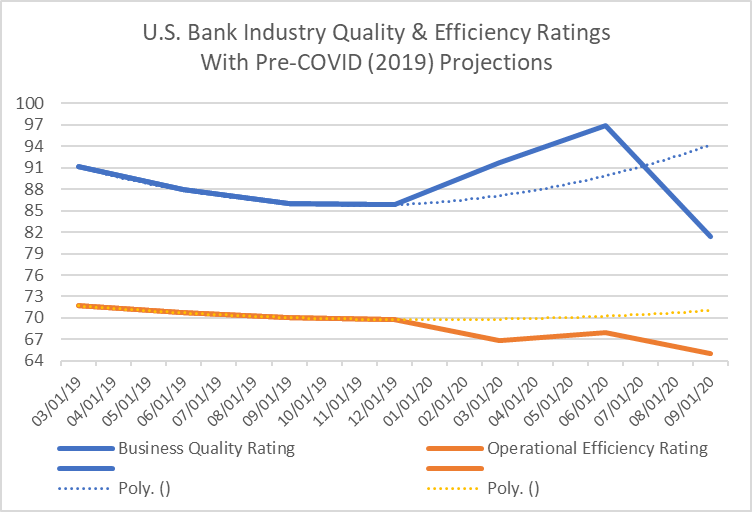

Although the bank industry experienced a dramatic change in performance in 2020 due to COVID 19 and the related economic shutdown, the industry’s pivotal role in the distribution and application of the several government relief programs appears to have helped soften the blow. Hoeg & Company, Ltd. has previously noted that the impact of the economic shutdown as seen in each of the three first quarters of 2020 using our Ratings of Business Quality and Operational Efficiency, but what would have the industry’s performance been without the shutdown?

Prior to COVID 19, the U.S. bank industry had been becoming progressively less operationally efficiently with diminishing quality books of business. Likely this trend was happening due to banks being in such a profit and growth friendly economic environment before COVID that they could capture additional growth and profit by accommodating previously unattractive business and the extra costs needed to service it.

Our ratings of bank Operational Efficiency and Business Quality showed this with respect to both efficiency and quality declining each quarter of 2019.Since 2008 the U.S. bank industry had been consolidating with fewer banks operating in the country each year while the economy had been growing, most significantly in recent years.The combination of fewer banks and an improving economy was good for most banks.Unfortunately, good times sometimes spawns a degree of complacency.Many banks in the industry started accepting lower efficiency in their operations, as well as, lower quality in their books of business to capture more business as the economy improved and grew.

For 2019, using our Ratings of Efficiency & Quality, we see the progression of the industry toward less efficient operations and lower quality books for business. The trend slowed toward the end of 2019, likely due to the upcoming Presidential election and the uncertainty such an event engenders.

Bank managers cannot be criticized for this trend. With less competition and growing demand, it would have been irresponsible to not seek growth and additional profits. With fewer banks and increasing business and personal financial activity due to the improving economy, banks would have been hard pressed to not accept business they previously might not have. Thus, to remain competitive for the business of their most attractive customers and to serve their new business they needed to increase capacity and improve services, incurring increased costs in the process.

Looking at 2020 we see that In Q1 the industry’s operational efficiency dropped more than for all of 2019 but increased business quality slightly above the level at the end of Q1 2019.

The improvement in business quality continued in Q2 2020 likely as a result of lower quality business accounts closing from individuals using their funds and some businesses failing. The banks, in response, appear to have realigned and reduced operating resources resulting in improved operating efficiency. Unfortunately, it appears the initial improvement in business quality in Q1 and Q2 and the improvement in operational efficiency in Q2 were not sustainable as the economic shutdown deepened in Q3.

The question that arises is, was the bank industry headed to this situation of reduced business quality and operational efficiency anyway and was the impact of COVID 19 actually a temporary benefit to the banks? Considering that all the federal government responses to support the economy during the pandemic necessarily ran through the banks placing funds in the hands of individuals and businesses in the form of cash payments and loans. Did the banks actually benefit from these actions such that the net impact on them was merely a temporary beneficial deviation on their prior trajectory to lower business quality and lower operational efficiency?

If we look at the trend in quality and efficiency for U.S. banks for 2019, before COVID 19, in parallel rather than in opposition to each other and we project forward we see that both were at an inflection point prior to 2020. Both business quality and operational efficiency were poised to improve, especially business quality. This was likely the case because economic improvement in certain areas had progressed so far that they were approaching their natural limits, such as unemployment. Improvements in certain areas of the economy could not continue to progress at the same high rates that had occurred in recent prior years and the expectation would be that improvements in the economy would slow. The slowing of improvements in some of the drivers of the economy, like unemployment, would naturally lead banks to seek to improve their books of business and reduce operating costs under the same logic that lead them to allow both to decline while economic improvement was at record high levels.

Looking at the projected performance of U.S. banks based on the pre-COVID period in comparison to the actual industry performance for the first three quarters of 2020, we see that, despite any temporary benefit from government programs to combat the impacts of the COVID shutdown, the banks have suffered a decline in both business quality and operational efficiency relative to where they would have been without the COVID shutdown and even relative to where they were before the shutdown.

It is doubtful that even the recently proposed (December 20202) COVID 19 relief bill from the federal government will suffice to overcome the declines in efficiency and quality for U.S. banks. This points to future poor prospects for financial results from the banks as their cost of doing business increases while the profit potential of their books of business declines. The banks in the U.S. are now facing a situation in which they will potentially be wasting assets through incurring ongoing operational inefficiency to sustain diminished quality business portfolios until such time as the economy recovers and regains the strong growth of recent years.

The questions that bank management must deal with now are:

1. How long will the shutdown and its associated economic decline continue?

2. How long can their bank exist with inefficient operations and a poor-quality book of business?

3. What options are there for their bank to assure that the answer to question 2 is greater than the answer to question 1?

For some banks, pursuit of higher quality business despite any increased costs will be best. For others, managing for efficiency in operations will be the key to survival and success. Thus, the real question is, which is best for their bank and its situation? Differences in strategy will likely be driven by bank size, geographic spread, business scope, current capital position and current level of operational efficiency and business quality. Some banks are much better than competitors and peers in one or both of the measures of efficiency and quality and can use those advantages to contend with the impacts of the COVID 19 shutdown. Those banks who are already behind in business quality and operational efficiency will likely need to consider much more dramatic changes and trade-offs in their strategy to deal with the impacts of the COVID 19 shutdown.

Ultimately, the bank industry, as a whole, has and will suffer from the impacts of the COVID 19 economic shutdown and those banks with plans to specifically address the challenges operationally and strategically will fare best.